Find Your Best Debt Consolidation Refinance Rates... Fast & Free!

Get an Accurate Rate Quote Today!

Find Your Best Debt Consolidation Refinance Rates... Fast & Free!

Get Pre-Approved Today and Shop with Confidence!

Debt Consolidation Refinance

A debt consolidation refinance can be a strategic financial move with Michigan Mortgage Solutions. Our debt consolidation refinance can help you save money by consolidating high interest consumer debt like credit cards with ease. This involves replacing your existing mortgage with a new one, typically at a lower interest rate or with different terms. This can lead to reduced monthly payments, shorter loan terms, and less interest paid towards your debts.

Why Choose Michigan Mortgage for Debt Consolidation Refinancing?

Our unique educational approach sets us apart by prioritizing transparency and empowerment for every borrower. We believe that an informed client is a confident client, which is why we break down complex mortgage concepts into easy-to-understand steps. This ensures that you not only feel comfortable with your debt consolidation refinance choices but also make decisions that align with your financial goals.

We guide you step by step through the refinance process, from the initial consultation to the final approval, ensuring that no question goes unanswered. Our team is dedicated to making sure you fully understand each phase, from rate quote to closing, while also identifying strategies to reduce your out-of-pocket expenses. By addressing potential challenges early and tailoring solutions to your unique situation, we help streamline what can otherwise be an overwhelming process.

Our ultimate goal is to match you with the best refinance program that fits your financial needs and future plans while making the experience as smooth as possible. We handle the details so you can focus on your homeownership journey with confidence and peace of mind. Our approach is designed to take the stress out of refinancing and replace it with clarity and support.

How Can Our Debt Consolidation Refinance Loans Benefit You?

At Michigan Mortgage Solutions, we focus on providing personalized mortgage lending services. Our experienced team works closely with you to understand your financial situation and goals, helping you secure a refinance loan that best fits your needs.

Our competitive rates and expert advice ensure you get the best deal possible. At the end of the day, our goal is to earn your mortgage business for life as most borrowers have a need for a mortgage more than just one time. If we do our job right you will always think of Michigan Mortgage Solutions for your mortgage lending needs.

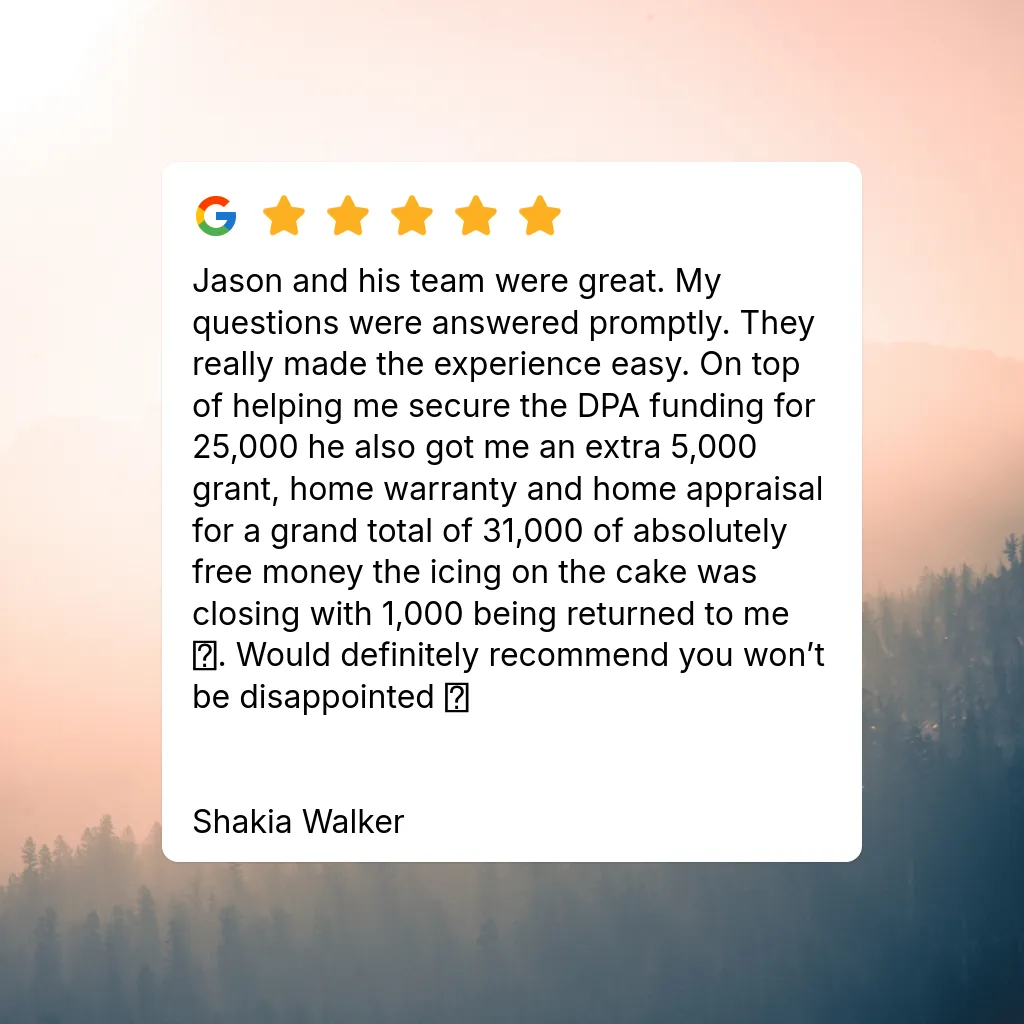

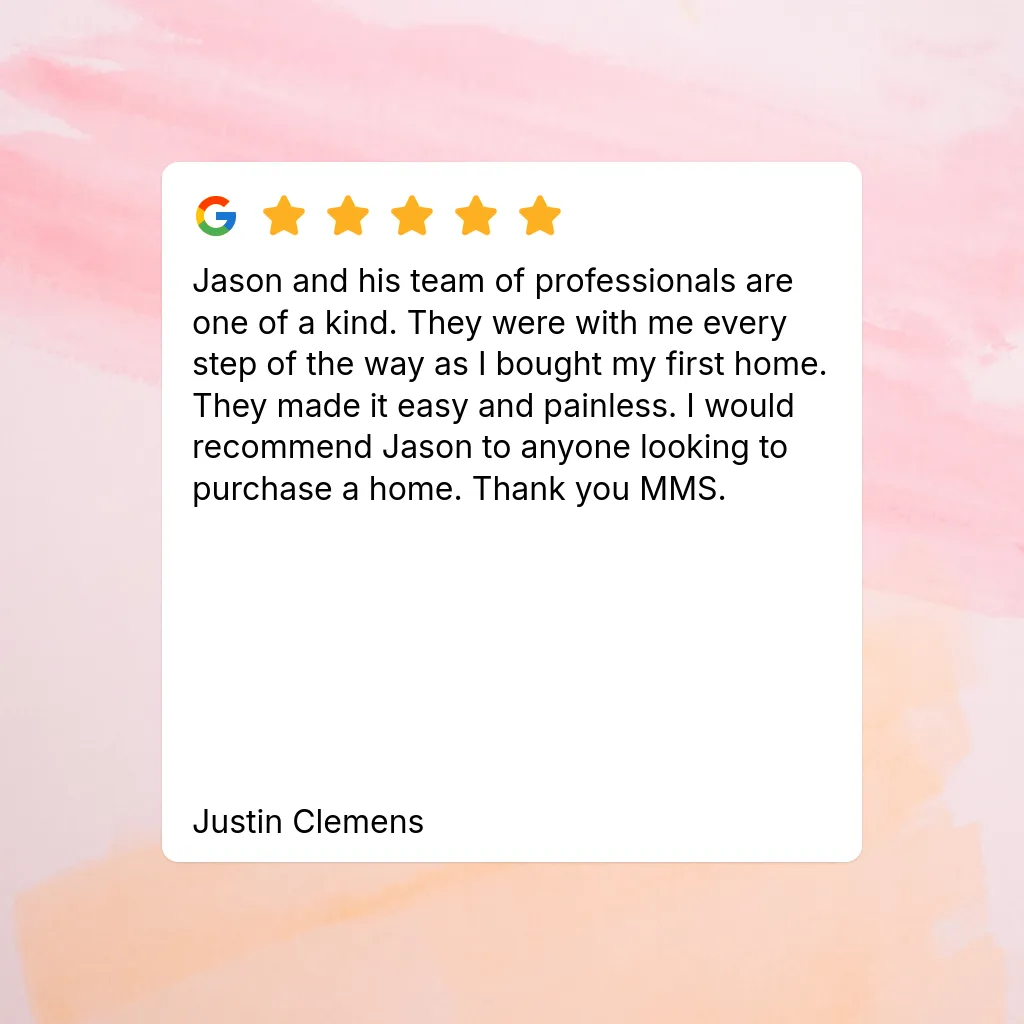

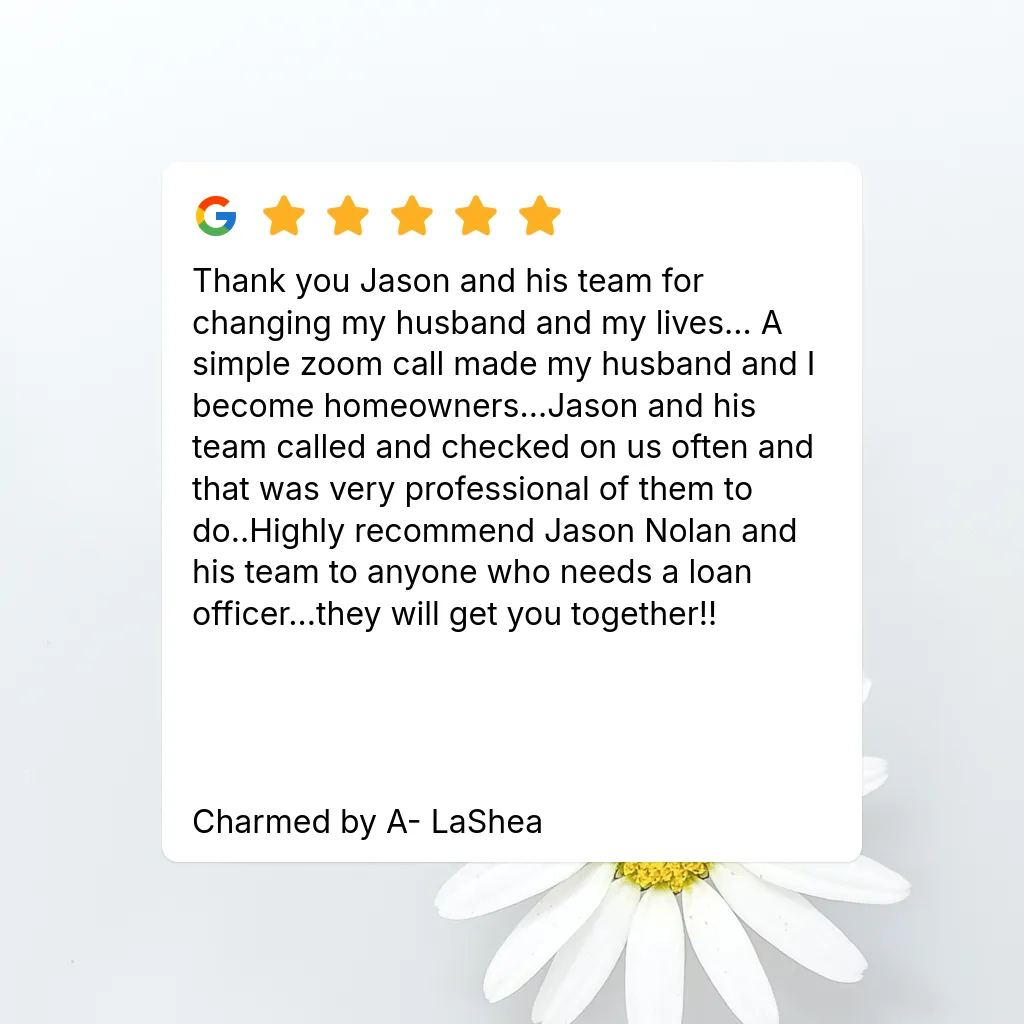

Recent Mortgage Reviews

Recent Mortgage Reviews

Our Process For A

Debt Consolidation Refinance

Step 1 - Complete Our Quick & Easy Home Loan Quiz

In just 45 seconds, you’ll provide the basic info needed to start your mortgage journey—no hard credit pull or long forms required. It's a fast, simple way to see your options and take the next step toward your homeownership or refinance goals.

Step 2 - Book Your Free Home Loan Consultation

Scheduling your consultation is quick and easy—just pick a date, select a time, and confirm your contact info. In minutes, you'll be all set to chat with a mortgage expert who will guide you through your options and answer all your questions.

Step 3 - Get Pre-Approved With An Accurate Rate Quote

Our pre-approval process is designed to give you clear, accurate details from start to finish. First, we run a soft credit check (so your score stays unaffected) and verify your income. Next, you provide a property address of interest, and we create a personalized financial breakdown using precise numbers based on your loan program and the property details.

Our Process For A

Debt Consolidation Refinance

Step 1 - Complete Our Quick & Easy Home Loan Quiz

In just 45 seconds, you’ll provide the basic info needed to start your mortgage journey—no hard credit pull or long forms required. It's a fast, simple way to see your options and take the next step toward your homeownership or refinance goals.

Step 2 - Book Your Free Home Loan Consultation

Scheduling your consultation is quick and easy—just pick a date, select a time, and confirm your contact info. In minutes, you'll be all set to chat with a mortgage expert who will guide you through your options and answer all your questions.

Step 3 - Get Pre-Approved With An Accurate Rate Quote

Our pre-approval process is designed to give you clear, accurate details from start to finish. First, we run a soft credit check (so your score stays unaffected) and verify your income. Next, you provide a property address of interest, and we create a personalized financial breakdown using precise numbers based on your loan program and the property details.

Michigan Mortgage Solutions Services

Michigan Mortgage Solutions Services

Things to Know About

Mortgage Lending

Not All Mortgage Providers Are Created Equal

When it comes to mortgage lending, not all providers offer the same level of service or access to loan options. Banks and direct lenders may only provide their own limited set of mortgage programs, which can restrict your ability to find the best terms for your financial situation. They also mainly work bankers hours which may hinder your ability to speak with your lender after hours or on the weekend.

In contrast, working with a mortgage broker can significantly expand your options. Brokers have access to a wide network of lenders, which allows them to shop for competitive interest rates and loan programs tailored to your unique needs. This flexibility often results in better terms, lower fees, and a more personalized experience compared to traditional lending institutions.

Plus, at Michigan Mortgage Solutions we make ourselves available after hours and on weekends when our clients need us. The majority or purchase deals usually happen after hours or on the weekend so this is key to making the best offer.

The Importance of Avoiding a Hard Credit Pull Too Early in The Pre-Approval Process

A common misconception in mortgage loans is that a hard credit inquiry is required to get pre-approved, but this isn’t always true. Experienced mortgage professionals can use soft credit pull data to estimate your eligibility without impacting your credit score. This approach prevents unnecessary hard inquiries, which can lower your credit score and trigger unwanted outreach from competing lenders who purchase trigger leads.

By waiting to authorize a hard credit pull until you're ready to lock in a rate, you not only protect your credit but also maintain control over your mortgage process without unnecessary distractions or sales pitches from other lenders.

Why Online Reviews Matter When Choosing a Mortgage Lender

Before committing to a lender, it's essential to research online reviews to understand their areas of expertise. Many lenders focus heavily on refinance loans, and their customer service for home purchases—especially for first-time buyers—may not be as seamless.

If most reviews highlight positive experiences with refinancing but have limited mentions of purchase transactions, it could indicate a less-than-ideal fit for someone navigating the complexities of buying their first home. Look for reviews that mention successful purchases, responsiveness, and support throughout the home-buying process. This due diligence helps ensure you choose a lender experienced in your type of loan, leading to a smoother and more satisfying mortgage experience.

Work with Michigan Mortgage Solutions

At Michigan Mortgage Solutions, we’re dedicated to helping you navigate the mortgage process with ease and confidence. Our team combines years of expertise with a client-first approach to find the best mortgage program for your unique financial situation. Whether you're a first-time homebuyer or looking to refinance, our goal is to simplify the lending experience and secure the best terms for you.

We invite you to schedule a free home loan consultation to discuss your options and take the first step toward achieving your homeownership goals. Let us show you how personalized service and expert guidance can make all the difference in your mortgage journey.

Things to Know About A

Debt Consolidation Refinance

Things to Know About A Debt Consolidation Refinance

Not All Refinance Options Are Created Equal

When it comes to refinancing, not all options offer the same benefits or flexibility. Many lenders provide limited refinancing programs that might not cater to your unique needs, especially if you’re looking to consolidate high-interest debt. Traditional banks often have rigid requirements and limited availability, making it harder to find the best refinancing solutions.

Working with a mortgage broker, like Michigan Mortgage Solutions, opens the door to a broader range of options. Brokers have access to multiple lenders, allowing them to find competitive rates and customized programs for debt consolidation refinancing. This flexibility can help reduce your overall monthly payments and simplify your financial obligations.

At Michigan Mortgage Solutions, we are available after hours and on weekends to ensure that your refinancing needs are met when it’s convenient for you.

The Benefits of Debt Consolidation Refinance

Debt consolidation refinance offers several key advantages for homeowners:

Lower Monthly Payments: By combining high-interest debts into one mortgage payment, you can lower your overall monthly expenses.

Reduced Interest Rates: Mortgage rates are typically lower than those for credit cards or personal loans, saving you money over time.

Streamlined Payments: Consolidate multiple debts into a single, manageable payment.

Potential Tax Benefits: Mortgage interest may be tax-deductible, unlike interest on credit cards or personal loans.

These benefits make debt consolidation refinance a powerful tool for simplifying finances and improving cash flow.

Eligibility for Debt Consolidation Refinance

To qualify for a debt consolidation refinance, you’ll need to meet certain requirements:

Sufficient Equity: Most lenders require you to have at least 20% equity in your home.

Creditworthiness: While less stringent than other loans, a good credit score can improve your terms.

Debt-to-Income Ratio (DTI): Lenders prefer a DTI ratio below 43%, though exceptions may apply.

Our team at Michigan Mortgage Solutions can assess your eligibility and recommend the best refinancing solution for your financial goals.

How Debt Consolidation Refinance Works

The process involves replacing your existing mortgage with a new one that includes the amount needed to pay off your high-interest debts. After refinancing, you’ll make a single payment for your mortgage rather than managing multiple payments across different debts. This simplifies your finances while potentially saving you money on interest.

Why Choose Michigan Mortgage Solutions For Your Debt Consolidation Refinance?

At Michigan Mortgage Solutions, we specialize in debt consolidation refinancing and work with a wide network of lenders to find the best solutions for our clients. Whether you’re dealing with credit card debt, personal loans, or other financial burdens, we can help you refinance with confidence.

Schedule a free consultation today to explore how debt consolidation refinance can simplify your finances and save you money.

Contact Us

Service Hours

Social Media

Monday - Friday: 9:00 AM - 6:00 PM

Saturday: 9:00 AM - 12:00 PM

Sunday: Closed

More Locations We Serve

All Rights Reserved Corporate NMLS 136972

Contact Us

(248) 963-1894

35 W Huron St #301

Pontiac, MI 48342

Service Hours

Monday - Friday: 9:00 AM - 6:00 PM

Saturday: 9:00 AM - 12:00 PM

Sunday: Closed

Social Media